Do you really want to remodel your home but aren’t sure if it’s financially possible? Thinking you might have to move instead?

Don’t list your beloved home just yet — we’ve got good news. There are plenty of options for financing a home renovation, whether you want to revamp your first floor or your entire home.

At COCOON, we’re here to guide you through every stage of the process, including helping you choose the ideal layout for your budget. Let’s explore the world of home remodel financing together.

While we all love the Philly suburbs, we’re all different when it comes to finances. That’s why the best loan option for your remodel depends on your current needs and financial history.

Before calling your bank or broker, ask yourself the following questions:

It’s alright if you don’t have all the answers or exact amounts. You can take your best guess to get the conversation rolling with your loan officer, and they’ll take it from there. An appraiser will also determine your home’s after renovation value (ARV) before the remodel begins.

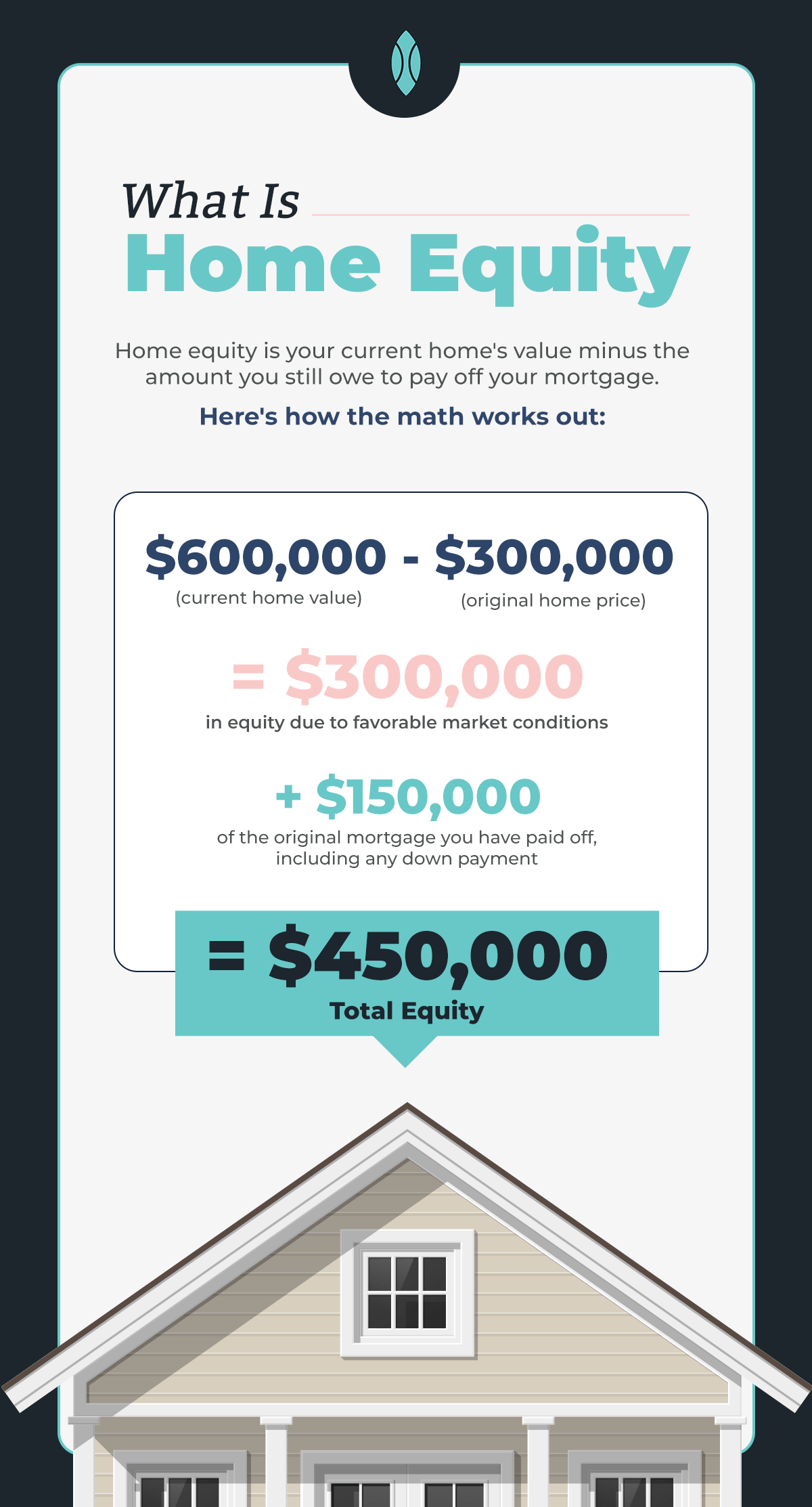

Home equity is your current home’s value minus the amount you still owe to pay off your mortgage. Your home equity will go up as your property value increases due to market conditions. You can use equity as collateral to secure a variety of loans and finance your remodel.

Let’s say you bought your house 10 years ago for $300,000. Now it’s worth $600,000, and you still owe $150,000 having paid off $150,000 of your original mortgage, including any down payment. That leaves you with $450,000 in home equity. Here’s how the math works out:

$600,000 (current home value) – $300,000 (original home price) = $300,000 in equity due to favorable market conditions + $150,000 of the original mortgage you have paid off, including any down payment = $450,000 total equity

Put another way, you can take the $600,000 that your home is currently worth, and subtract the $150,000 you still owe the bank for your original mortgage to get the $450,000 in equity.

Thinking about financing a bathroom remodel or home addition? Those renovations won’t just make you love your house more — they can also boost your home’s value, which may help you secure more financing for your remodel.

This is where ARV comes in. ARV stands for After Remodel Value. Simply put, this is the estimated value of your home after it’s been renovated. If you haven’t had a chance to build much equity, your home’s ARV can come in handy when getting a loan. At COCOON, we will collaborate with your loan officer as well as the appraiser to determine this number before we begin your renovation.

There are a lot of different ways to finance a remodel, and each has pros and cons. The one you choose comes down to your financial goals. Here are four of the most common options:

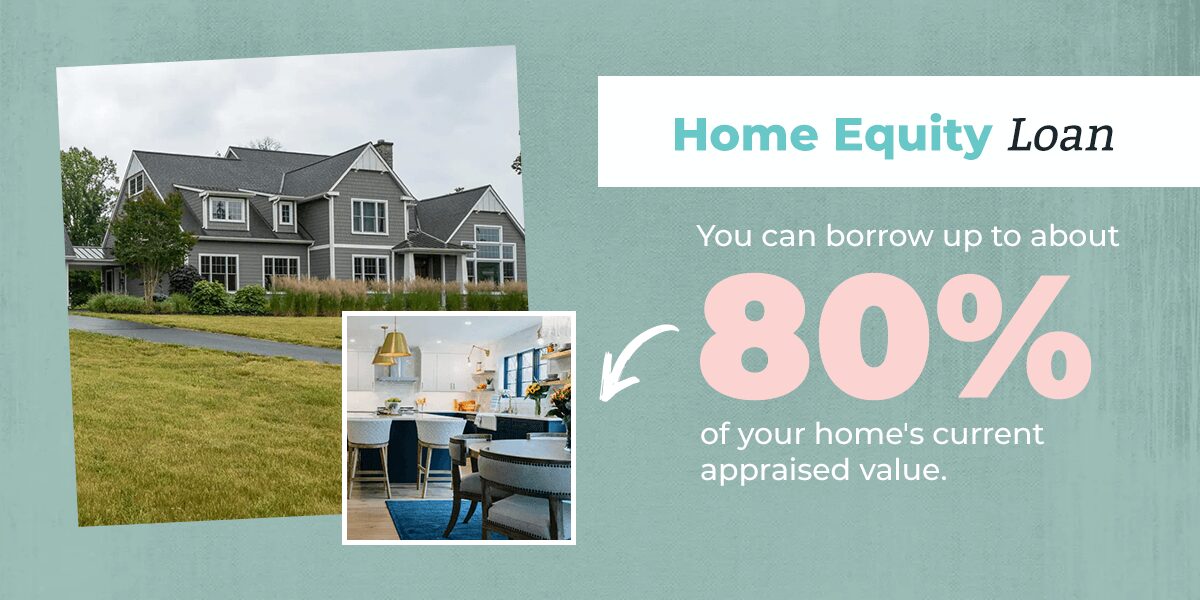

A home equity loan lets you use the equity you’ve built on your house as collateral. These loans usually have fixed interest rates that are often lower than those offered by other loans and credit cards. The average interest rate for a home equity loan is around 8%.

With a home equity loan, you’ll get a lump sum upfront, which you can put toward your remodel right away. The amount you can get varies by lender, but generally, you can borrow up to about 80% of your home’s current appraised value.

A home equity loan might be a great option if you prefer to make fixed payments each month. On the downside, you’ll start paying interest on the lump sum from day one. This is unlike using credit, which spreads out the amount you borrow.

A home equity line of credit (HELOC) lets you borrow against your home’s equity. Rather than providing a lump sum right away, a HELOC is more like a credit card. You can take money out of a HELOC as needed, up to a set limit. This option usually doesn’t have a fixed interest rate, so rates can go up or down.

With a HELOC, you can borrow as needed. You won’t be locked into the same monthly payment, and you’ll pay interest only on what you use.

A cash-out refinance is a way to refinance your mortgage. It allows you to pay off your mortgage with a larger loan and keep the extra cash for your remodel. Like home equity loans and HELOCs, you can usually borrow up to around 80% of your home’s value.

If your home is currently worth $500,000, the most you can borrow will be $400,000. With that in mind, let’s say you have a $500,000 home and still owe $200,000 on your mortgage. After paying off your mortgage, you can cash out $200,000 from the $400,000 loan to put directly toward your renovation.

For this option to make sense, you’ll need at least 20% equity in your home. If you have that, you might choose a cash-out refinance to keep your mortgage and remodeling loan under one payment. Regarding interest rates, they can be fixed or variable with this option and are generally lower than personal loans or credit cards.

Let’s go back to ARV. Unlike the other financing options above, a renovation loan allows you to borrow based on ARV, not your current home equity. These loans let you finance or refinance your home and pay for the cost of your remodel in one package.

A renovation loan can be a good choice if you’re a new homeowner and don’t have much equity to support a major remodel or want to renovate your home as soon as you move in — for example, if you fall in love with a fixer upper.

Renovation loans include:

Whether you dream of more space, made-for-your-family functionality or a style that truly reflects your personality, you have options for financing your remodel. At COCOON, we’re all about helping you realize your home’s potential and making it happen. We’re happy to help you determine your options based on your budget and needs, and we’ll do our absolute best to minimize challenges and guide you through making the right decisions.

If you’re ready to explore how you can transform your home, let’s start a conversation! Give us a call today.